FAQ’s on Non-Banking Financial Company (NBFC)

09 Dec, 2020

Here are FAQs on Non-Banking Financial Company-

Q.1: What is Non-Banking Financial Company (NBFC)?

Ans.: NBFC is a Non-Banking Financial Company which the principal business of which is:

- lending money or

- investing in shares/stocks/bonds/debentures or

- leasing hire purchase, or

- doing insurance business, chit business or

- Receiving deposits under any scheme or arrangement.

Note: NBFC is regulated by Reserve Bank of India.

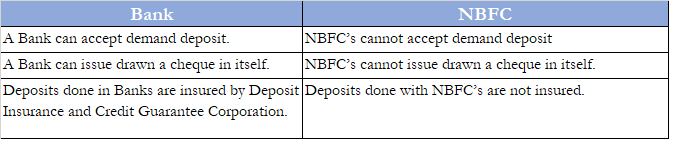

Q.2: Is Non-Banking Financial Company (NBFC) similar to Bank?

Ans.: The difference between an NBFC and a Bank is:

Q.3: What are the types of Non-Banking Financial Company (NBFC)?

Ans.: There are 2 types of NBFC’s, and they are:

- Deposit-taking NBFC’s.

- Non- Deposit-taking NBFC’s.

- Deposits Taking Non-Banking Financial Company (NBFC): There are mainly three types of the deposit accepting NBFC’s they can be explained as under:

- Loan companies,

- investment companies,

- asset finance companies.

There are some criteria’s which are required to be fulfilled by deposit-taking NBFC’s:

- They should have a net owned fund of Rs. 2 Crore.

- They should mandatorily get investment credit rating from any authorized credit rating agency for being eligible to accept deposits from people.

- Non- Deposit taking NBFC: These are the NBFC’s which cannot accept the deposit. They can only lend but cannot accept deposits from public other than paying back of the borrowed money. These types of NBFC’s generally depends on Banks, Corporate Houses, and Private Equity Firms, etc. for taking deposits.

Non-Banking Companies are further classified on the basis of their size.

Q.4: Is every business is allowed to carry on the business of NBFC?

Ans.: The following business cannot be registered as NBFC:

- Any institution whose principal business is of agriculture.

- Or any business who is engaged in industrial activity.

- Or any institution which is engaged in purchase or sale of any goods (other than securities).

- Or which is providing any services.

- Or which is engaged in sale/purchase/construction of the immovable property.

- Or any other company whose principal business is receiving deposits under any scheme or arrangement in one lump-sum or in installments by way of contributions or in any other manner.

READ NBFC-MFIs Top Micro-Credit Providers in India: Industry Report

Q.5: What are the requirements to register as an NBFC?

Ans.: As per the rules & regulations of Reserve Bank of India Act [1] , 1934 “No company can commence the business of NBFC unless it has obtained the certificate of NBFC registration and having a net owned fund of Rs. 2 Crore”.

For registering as an NBFC an application to the Regional Office of RBI should be made along with the required documentation.

Q.6: What are the reasons for the growth of NBFC?

Ans.: Reason for the growth of NBFC:

- NBFC has the ability to understand the customer’s profile and offer the best product according to the customers need.

- They offer competitive interest rates.

- Provide flexible repayment scheme and extended loan tenure.

- A minimum number of documents are required at the time of providing financial assistance as compared to banks.

- Loan seekers have flexible eligibility criteria.

Q.7: What is the time period for which NBFC can accept deposit?

Ans.: A time period has been provided regarding the maximum and minimum time limit for which NBFC can accept the deposit.

Minimum time period: 12 months.

Maximum time period: 60 months.

It is the discretion of deposit accepting NBFC that it can pay back the amount of deposit before its maturity period but such deposit cannot be paid back before 3 months from the date of its acceptance.

If the deposit is paid back after 3 months but before 6 months of its acceptance no interest will be paid.

But if the deposit is paid back after 6 months of its acceptance but before the maturity period then interest shall be paid but that interest shall be lower than 2% of the contracted rate.

READ Payment Gateway License in India

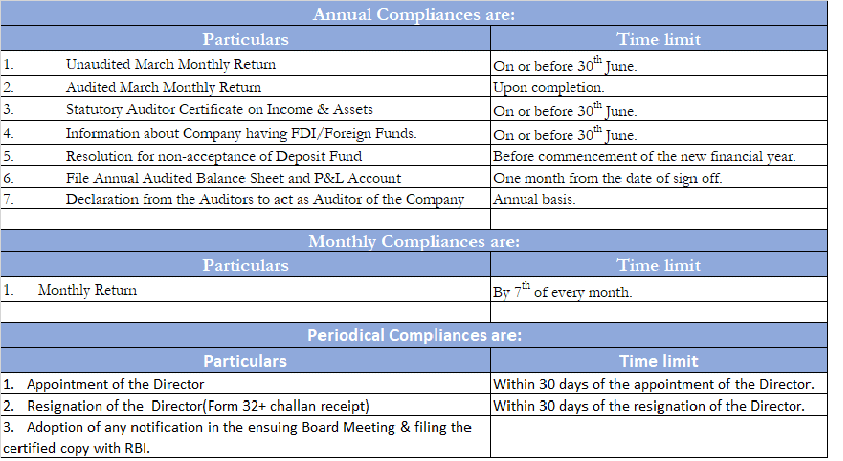

Q.8.: What are the compliances of Non-Banking Financial Company (NBFC)?

Q.9: What is Non-Banking Financial Company (NBFC) Takeover?

Ans: Likewise, any other company takeover of NBFC can also take place. The rules and regulations regarding the takeover of NBFC are regulated by the Reserve Bank of India. So, the takeover of NBFC means when any other NBFC acquires the other NBFC it is considered a takeover. Similarly, it can also be done in two different ways i.e. friendly takeover and a hostile takeover.